Monefit · Launch film

Monefit · Fintech · End-to-end design

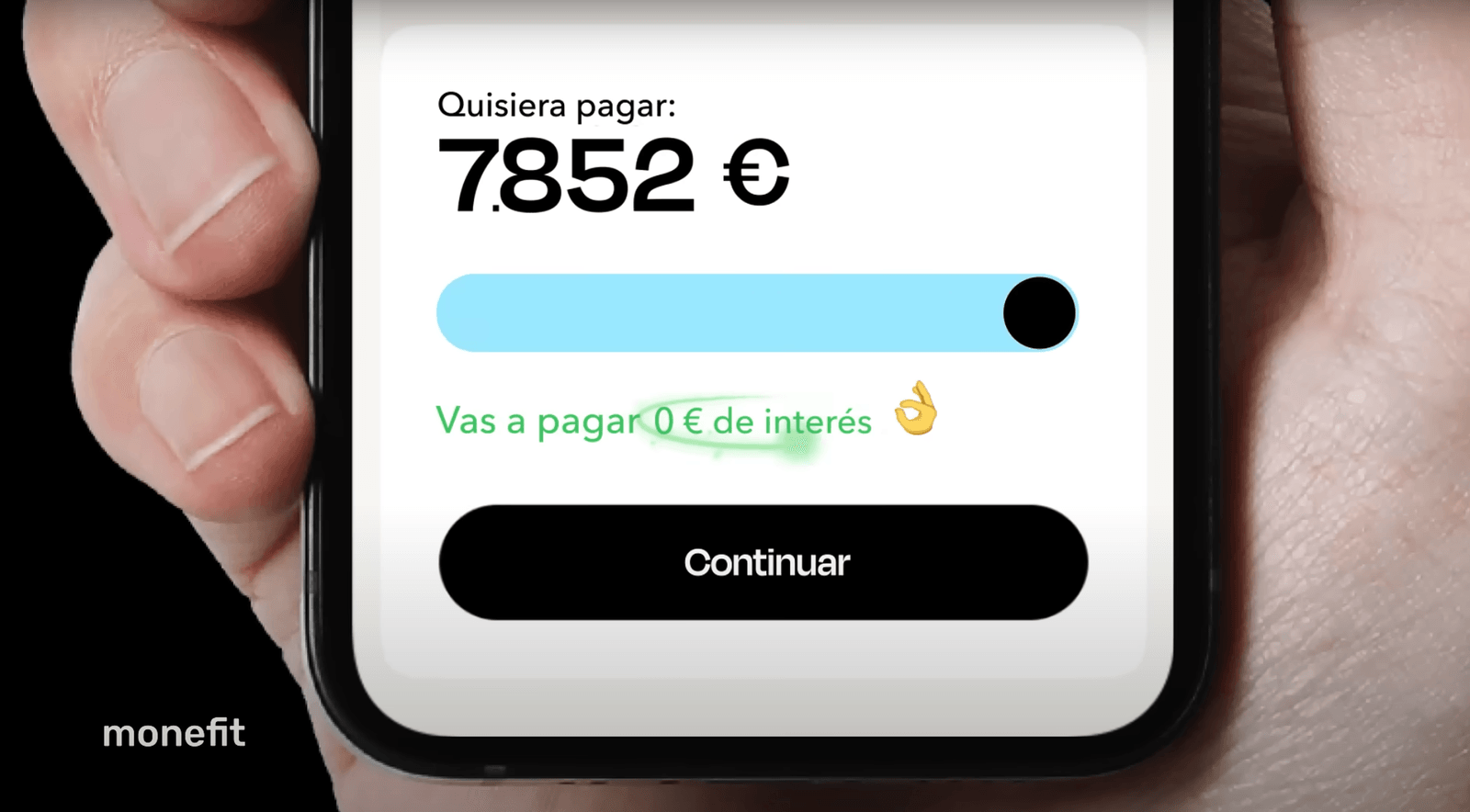

Monefit Credit subscription

I took a 0%-interest credit product from an empty Figma file to a live launch in Spain, then spent months making the funnel convert better, one drop-off at a time.

- ↑Onboarding completion

- 500Ads shipped in waves

- 8Markets templated

01 · Overview

A new way to borrow, built to be trusted

Monefit brought me in to design their Credit Subscription, a premium 0%-interest lending product for Spain, across mobile and desktop. Borrowing money is a nervous moment, so the job was to make it feel simple and honest, and to leave behind a template the other markets could pick up. I stayed on it from the first sketch through launch and beyond, running both the product design and the acquisition side.

Unlike a payday loan or a credit card, this thing charged 0% interest, had repayments you could see coming, and worked like a plain subscription. Which sounds great, and also meant nobody had ever heard of anything like it. In practice that meant:

- Explaining a brand-new product category to people who are rightly suspicious of free money.

- Keeping the lawyers happy without burying people in legal text.

- Building screens that eight other markets could reuse without redesigning everything.

- Getting signups at a sane cost, because every new user in finance is expensive.

02 · Research

Eight markets of data instead of months of research

We didn’t have months for a research phase, and luckily we didn’t need one: Monefit already ran in eight other markets. Old funnels, past launches and years of user behaviour became our baseline, so we could decide fast without guessing blind.

We also got on calls with people from the waitlist and asked why they’d signed up:

- The 0% interest was the headline draw; it made borrowing feel safe rather than shameful.

- The high credit limit mattered almost as much; people liked having room to breathe.

- And they split into two camps: some wanted the fastest possible flow, others wanted their hand held at every step.

That split ended up shaping the onboarding, the copy and the ad angles from day one.

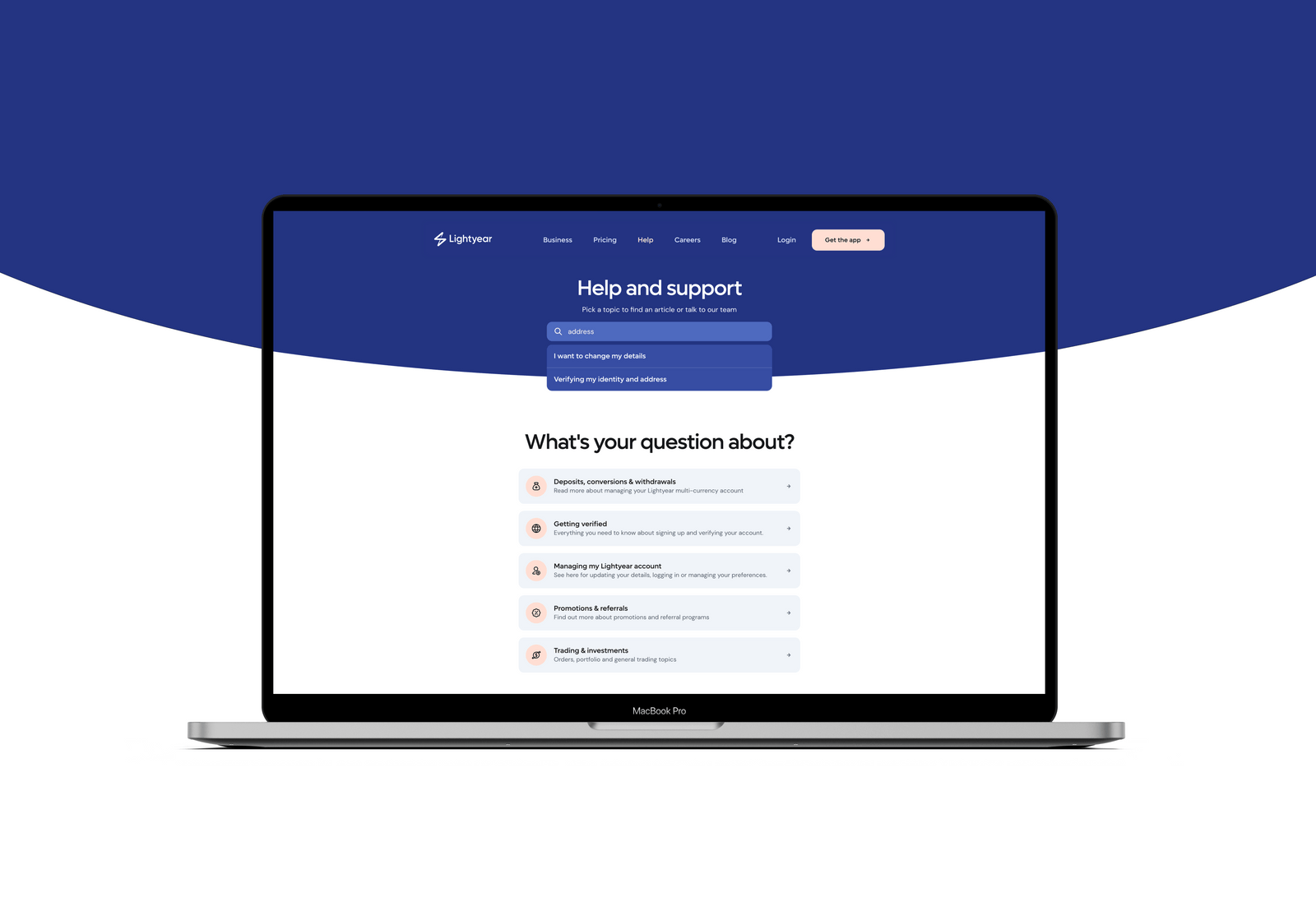

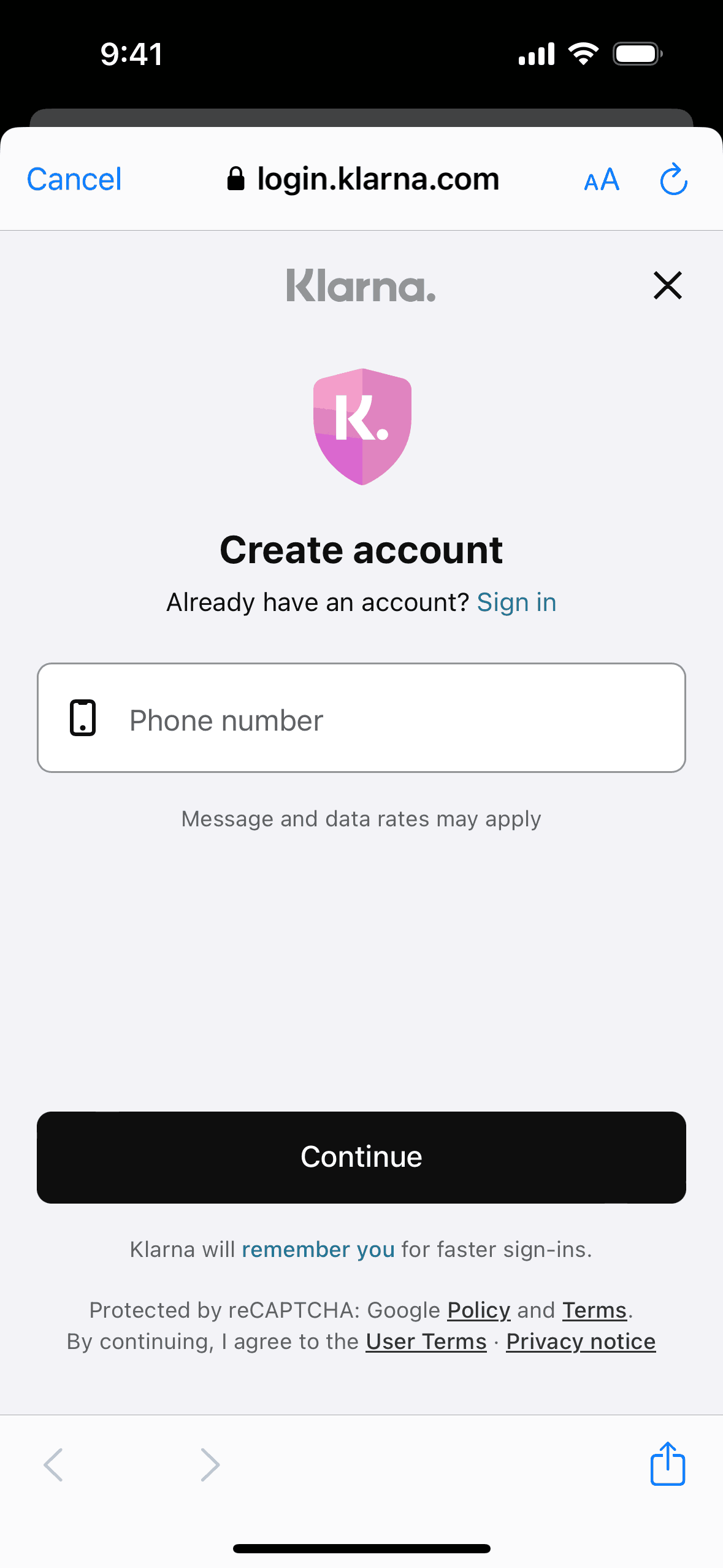

Klarna: the smallest possible first ask, a phone number

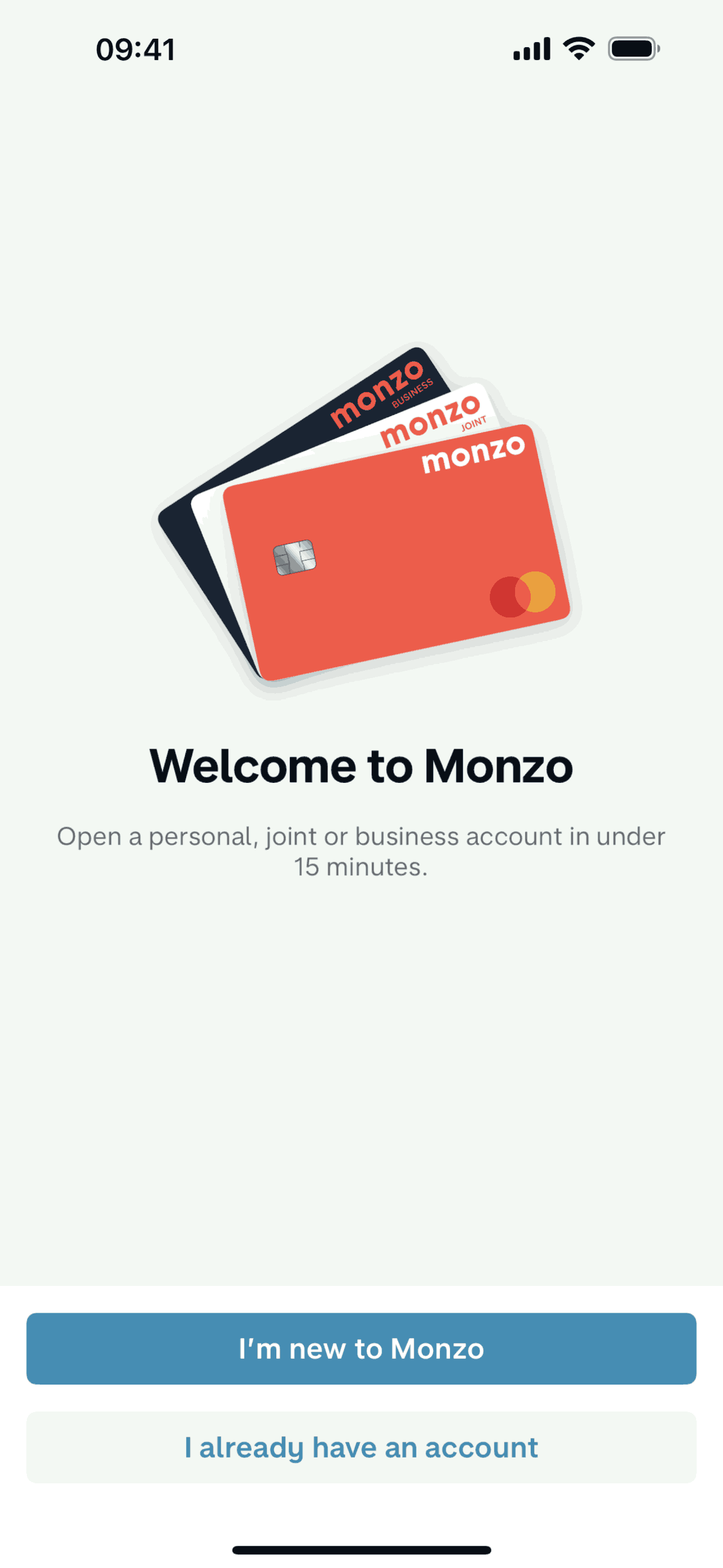

Monzo: a promise with a clock in it, reassurance built into the wait

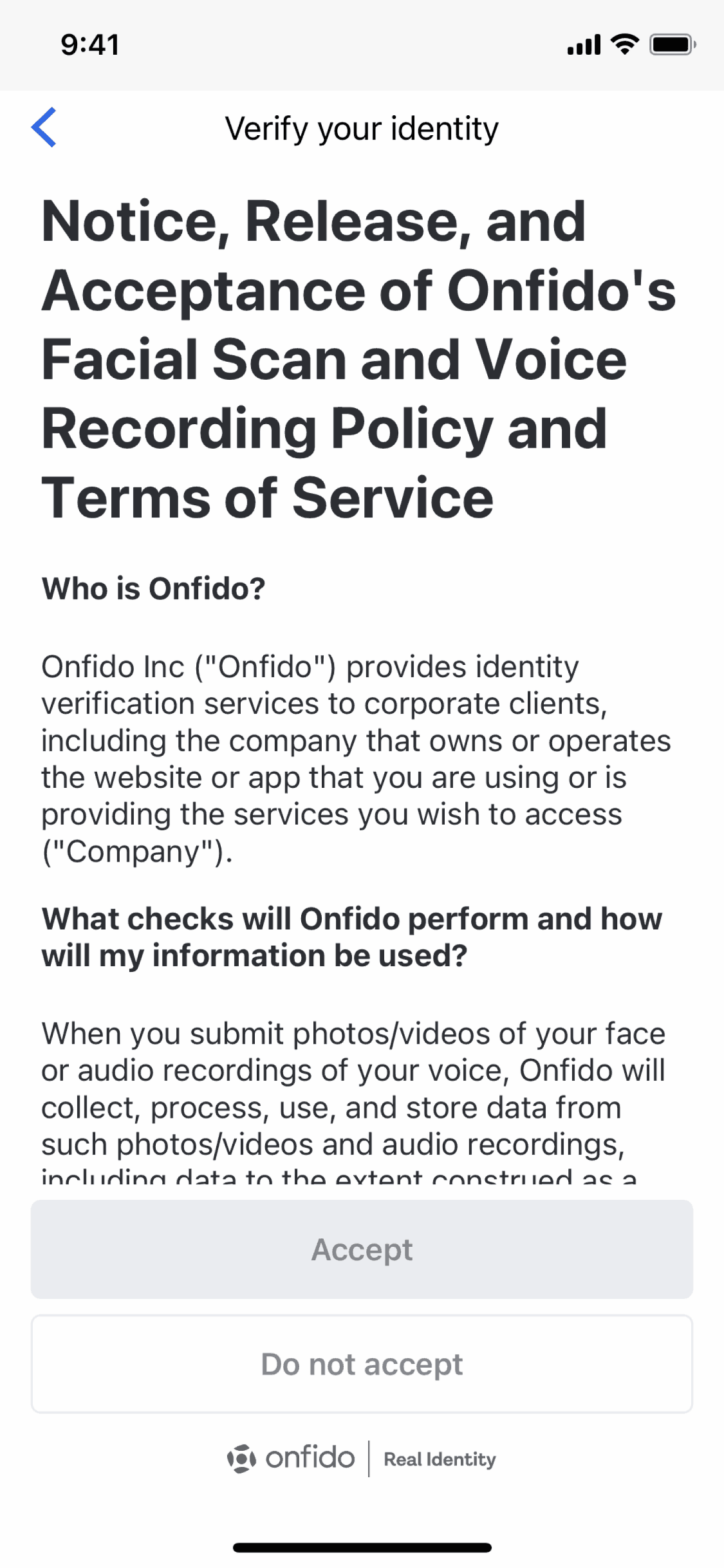

Revolut’s KYC step: the legal wall a credit product has to make painless

03 · The experience

Onboarding that earns the “confirm”

The whole onboarding flow is really one long exercise in removing friction while adding reassurance:

- Progress you can see: eligibility, documents, account setup, and always a sense of how far along you are.

- Short, plain copy exactly where the questions come up: what the subscription costs, when repayments land, what the legal bits actually say.

- Cutting steps after launch: we pulled product selection out of the flow entirely, and merged the loan agreement and the SECCI document into one step. Both changes showed up in completion within days.

Everything was built in reusable pieces, so the Spanish launch doubled as a starter kit for the other regions.

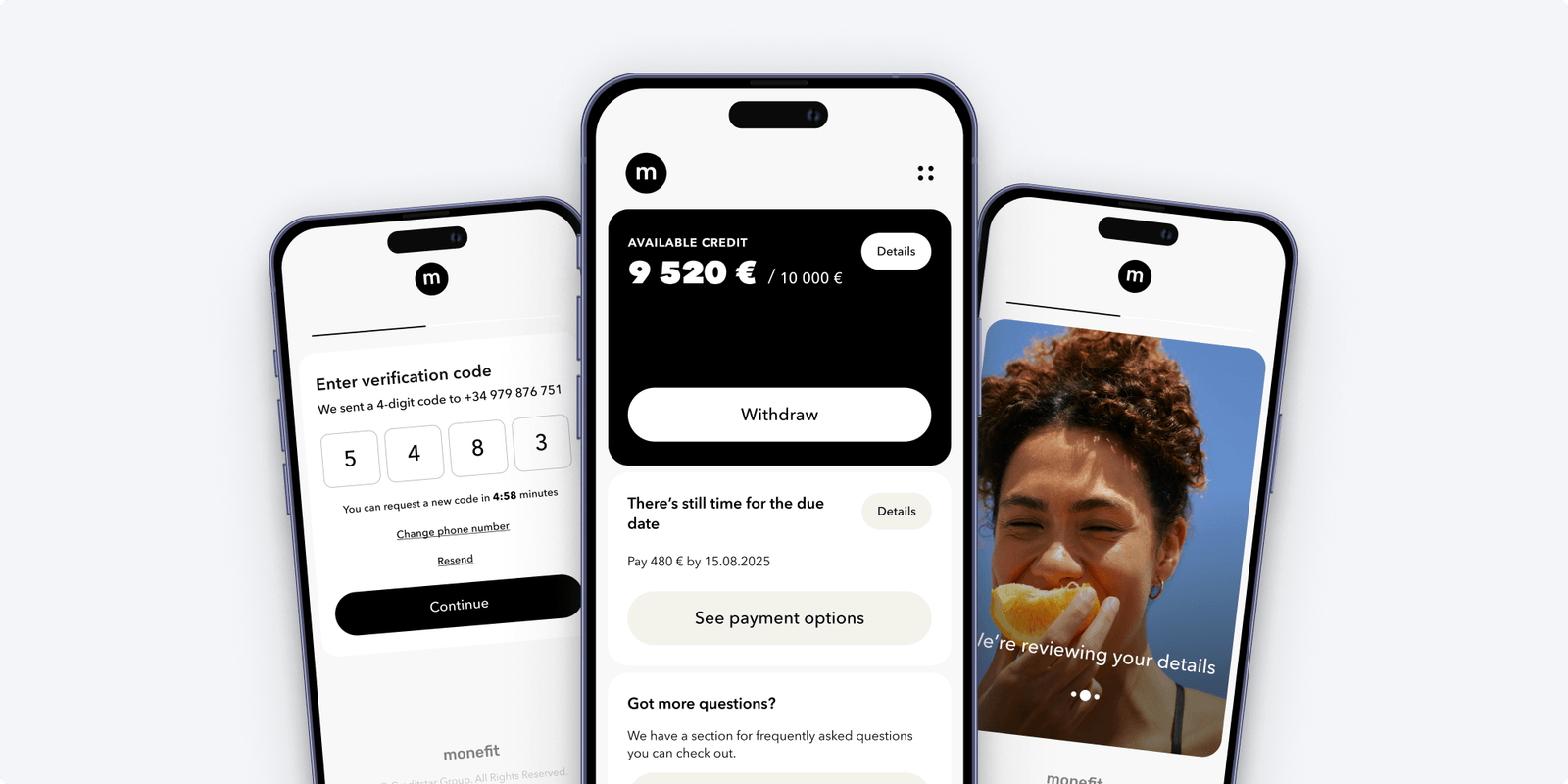

Dashboard and repayment

Inside the product, the dashboard answers the three questions a borrower actually has: how much can I still use, what do I owe, and when is it due. Repayments sit on a schedule you can read at a glance, and the transaction history uses labels a human would write. Nobody should ever be surprised by a repayment or a fee.

The biggest wins came after launch, by watching the funnel every day and quietly fixing what tripped people up.

04 · Acquisition

Product and marketing as one system

I designed 500 ads, shipped in waves of 100. The first hundred existed mostly to teach us; the numbers from those picked the next wave, where we doubled down on the angles that won. The messages came straight from those waitlist calls: 0% interest and a high limit, front and centre.

After launch we emailed the people who had started onboarding and stalled. A surprising share of them came back and finished, at a fraction of what a cold signup costs.

We also storyboarded and produced a launch video, half lifestyle film, half UI animation. Its look ended up steering the landing pages, the emails and most of what we shipped afterwards.

Post-launch iteration

I checked the funnel most mornings and shipped the fixes the same week: steps cut, legal documents rewritten until they read like language, email flows tightened. Onboarding stopped being a deliverable and became a living system that kept improving on real behaviour.

What I traded off

Where I chose speed over polish

The waitlist calls split people into two camps: the ones who wanted the fastest possible flow, and the ones who wanted their hand held. I resisted building two separate onboardings and designed one flow that could flex for both, because two funnels would have doubled the work and halved the learning. I also chose to launch before it felt finished and cut steps from live data, rather than guess the perfect flow up front. Watching real drop-off beat polishing in Figma every time.

05 · Outcome

What it added up to

Add the product work, the ads and the weekly fixes together, and the numbers moved:

- Onboarding completion climbed properly after the big flow cuts.

- Far fewer people bailed at the legal documents once two steps became one.

- The win-back emails rescued a healthy share of people we’d otherwise have lost for good.

- Every ad wave spent the budget harder as the losing angles got cut.

- And people told us they understood what they’d signed up for, which in lending is half the battle.

Key learnings

- Watching the funnel after launch beats polishing before it. Every time.

- Fast-lane people and hold-my-hand people can share one flow, if you design for both on purpose.

- Build the screens in pieces and the next market’s launch is mostly assembly.

- The ads and the product are one funnel; designing them together is what made either of them work.

- Ten calls with waitlist users taught us more than a formal research quarter would have.

06 · In the wild

Coverage and research

The brand has grown well past that first Spanish launch. Monefit now counts over 1.4 million clients across Europe, spread across two separate products: the credit subscription this case study covers, and SmartSaver, a separate savings product under the same brand that was named Best Investment Tech of the Year at the European Fintech Awards in 2025 and has independent reviewers tracking its numbers in public. The TechCrunch fintech coverage shows how crowded consumer credit became meanwhile, which is exactly why the funnel work mattered.

The research agrees with what our numbers kept saying. Baymard’s field-count studies show most checkout flows carry twice the form fields they need, the same disease KYC funnels suffer from. Built for Mars tears down real fintech onboarding flows step by step, and Growth.design does the same for conversion psychology, both are the closest thing to watching someone else’s funnel analytics.