Notes · Point of view · 8 min read

What most fintech onboarding gets wrong

Most fintech onboarding is a pitch delivered to someone who already said yes. The selling happened in the app store. What comes next should be the product keeping its promise, and usually it isn’t.

You’re marketing to the converted

Open almost any finance app for the first time and you get a slideshow. Money is easy now. Banking the world loves. Swipe, swipe, swipe, then finally a button that lets you in. The person doing the swiping searched for the app, read the reviews, downloaded it and opened it. They are as convinced as they will ever be. Every screen between them and their first real action is now cost, not persuasion.

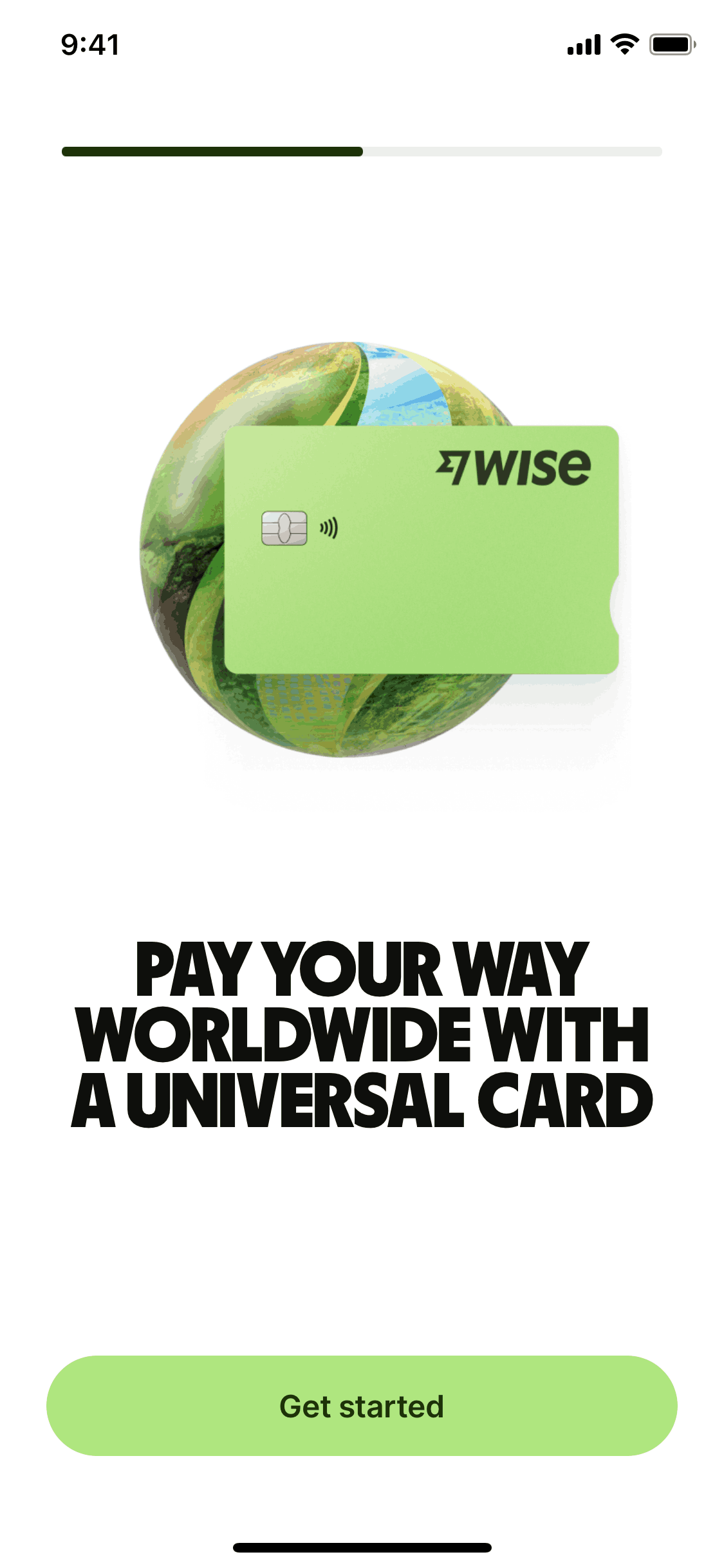

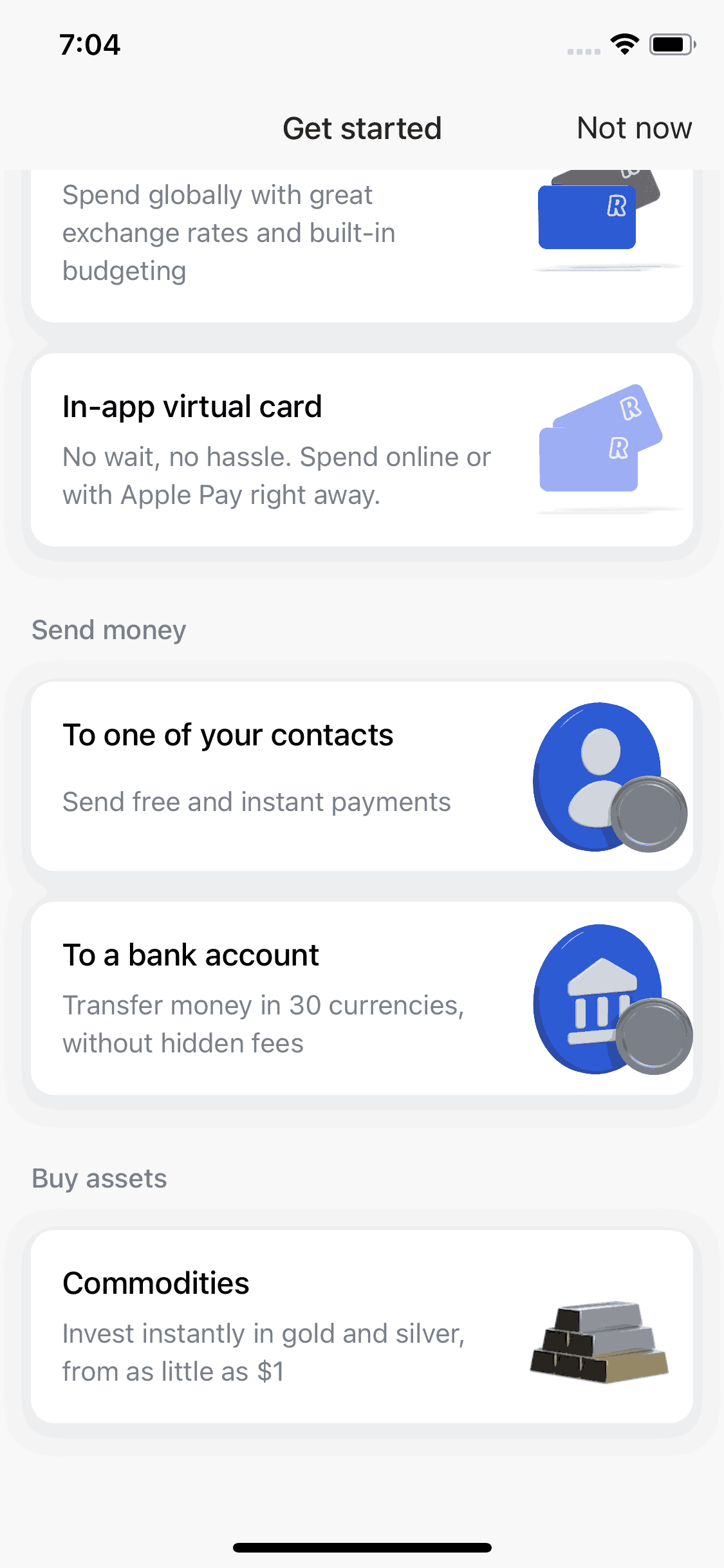

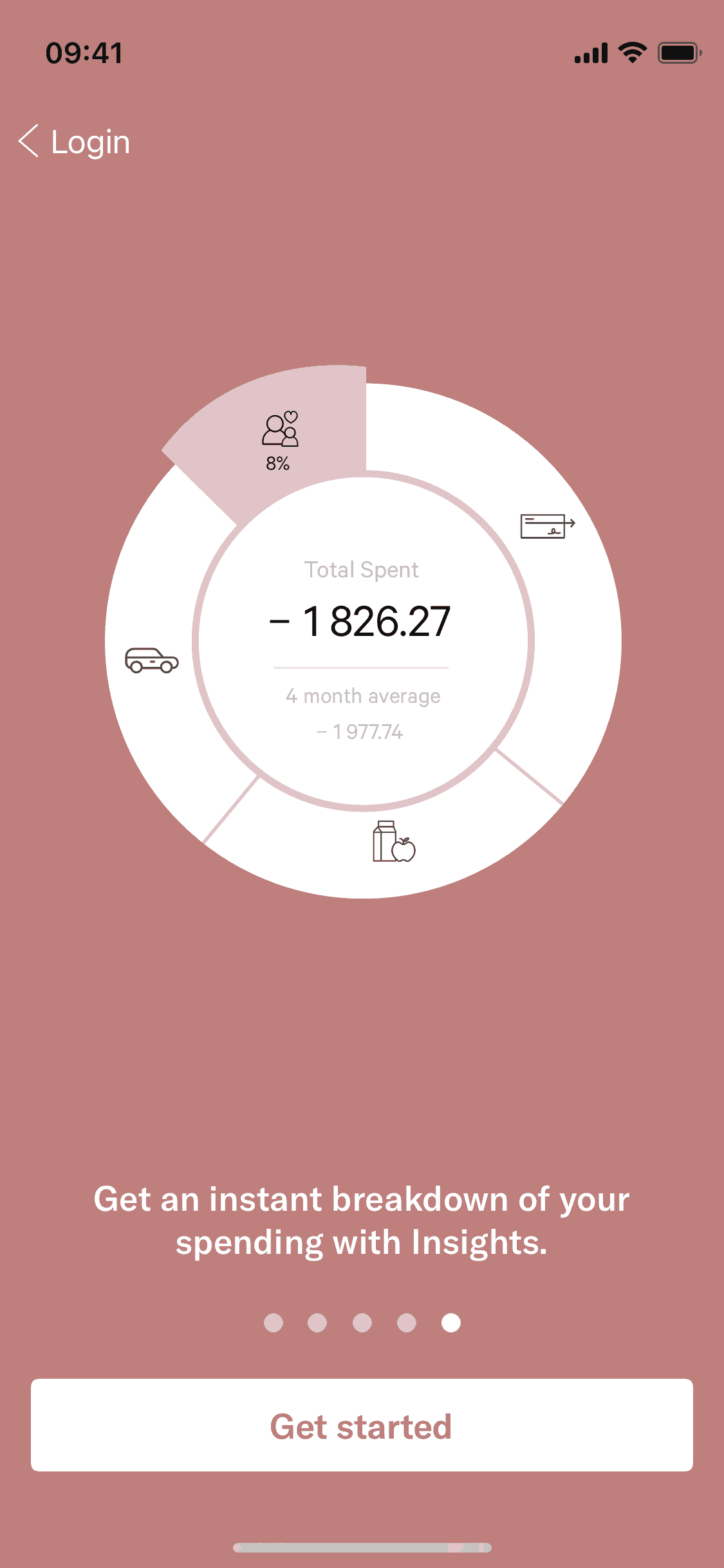

The three screens below show the range. Revolut gets to Login and Sign up on screen one, with the pitch as a headline rather than a detour: the right instinct. Wise leads with one concrete promise attached to a physical card. N26 gives a converted user a five-dot marketing carousel to swipe through, which is a beautiful way to say “we have nothing to ask you yet”.

Revolut: pitch as headline, actions on screen one

Wise: one concrete promise, one button

N26: a five-screen pitch for someone already sold

Nobody designs the KYC like they design the welcome

Here’s the uncomfortable part. The welcome flow gets the brand illustration budget, and then the actual onboarding begins: identity document, selfie, address, source of funds, politically exposed person questions. This is where real people actually give up, and it usually looks like a tax form that fell into the app from another company.

I’ve spent years inside these funnels, most recently rebuilding lending flows at Monefit, and the pattern repeats everywhere: the drop-off never happens on the pretty screens. It happens on the seventh form field, the document upload that fails without saying why, the “we’ll get back to you” dead end. That’s the part that deserves the design attention, because that’s where the money leaks.

Treat every KYC step like a landing page. Say why you’re asking. Show progress honestly, and never reset it. Let people leave and come back without losing everything. Write error messages like a human who wants the person to succeed. None of this is glamorous, which is exactly why it’s still rare.

And mind the silence at the end. Plenty of flows finish with “we’re reviewing your application” and then nothing: no timeline, no signal, no way to check. The person who was nervous on the seventh form field is now nervous with no form at all, which is worse. At Monefit we emailed people who had stalled mid-flow, and a surprising share came back and finished. I was glad those emails worked, but every one of them was an apology in disguise: the flow lost someone, the inbox went and got them back. If your win-back campaign performs brilliantly, that’s not a marketing win. That’s a design confession.

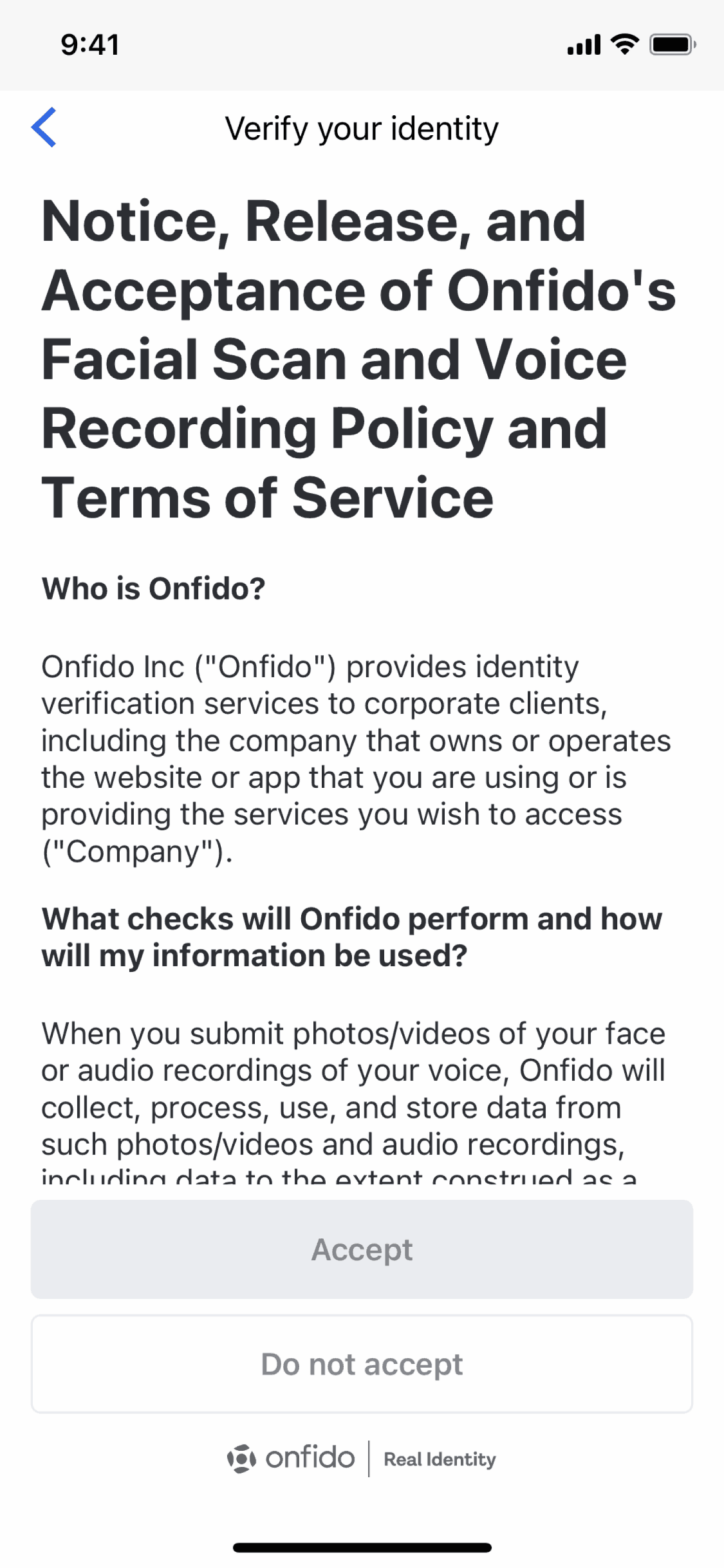

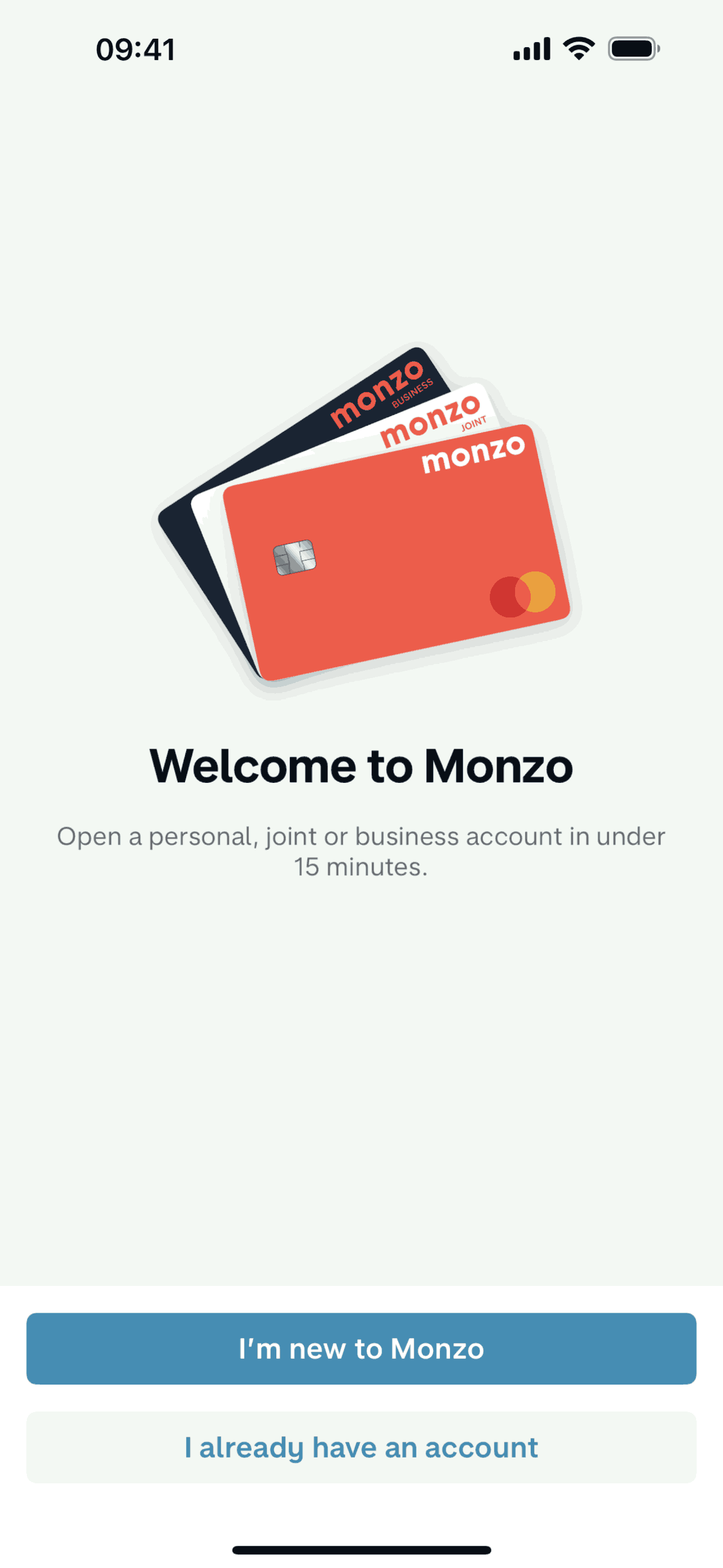

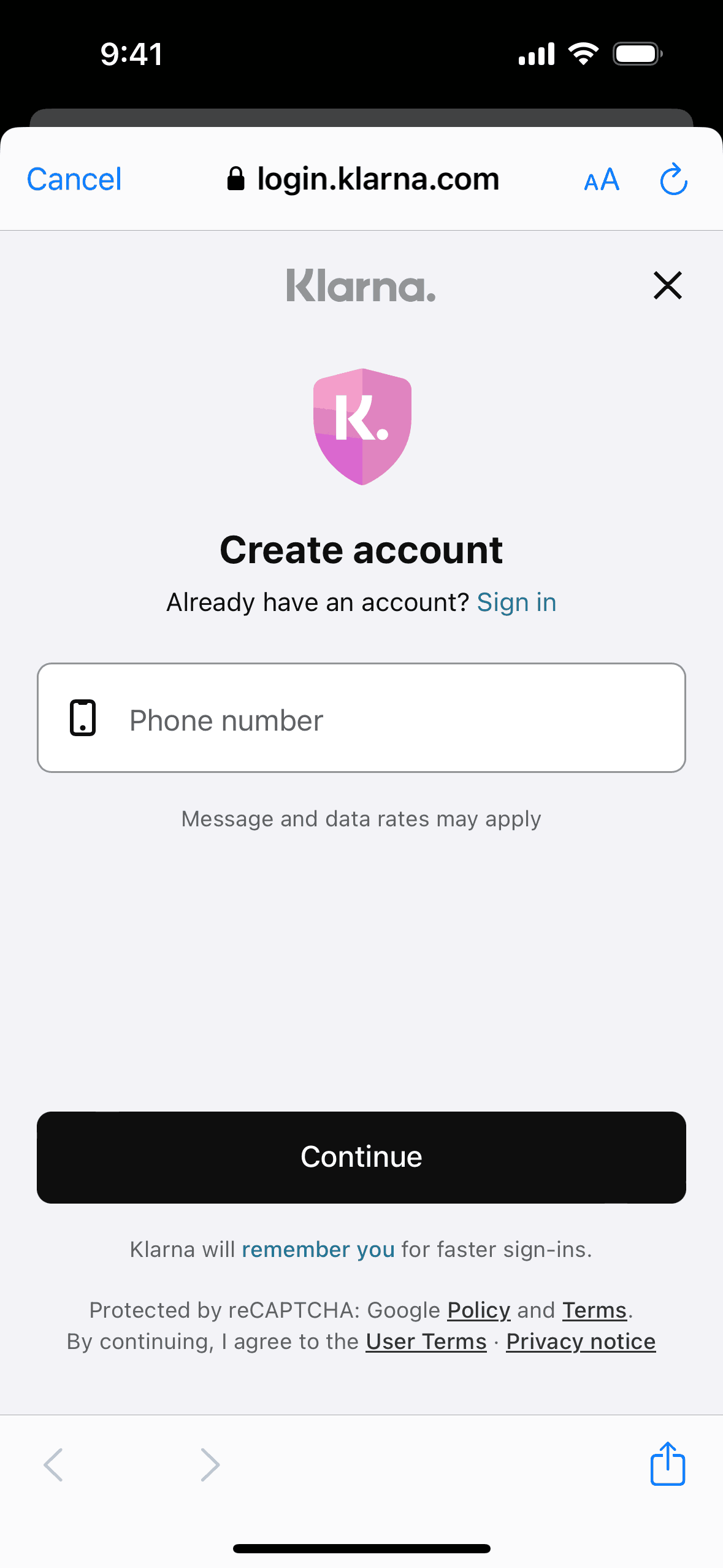

The screens below show the moment the mask slips, and two apps that keep it on. Revolut’s identity step hands you a wall of third-party legal text titled “Notice, Release, and Acceptance of Onfido’s Facial Scan and Voice Recording Policy”. That is a real screen a new customer meets minutes after “managing money is easy”. Monzo, by contrast, makes a promise with a clock in it: a full account in under 15 minutes, which reframes the entire interrogation as a countdown. And Klarna opens with the smallest possible ask, a phone number, and builds from there.

Revolut’s KYC step: another company’s legal wall, minutes after “money is easy”

Monzo: a promise with a clock in it. The interrogation becomes a countdown

Klarna: the smallest possible first ask, a phone number

The welcome screen has never lost a customer. The seventh form field has.

Show money before you ask for identity

The best fintech onboarding I’ve seen, and the kind I try to build, inverts the usual order. Let people see the product state first: the rate they’d get, the limit they’d have, what the dashboard will look like with their name on it. Give them something to lose. Then start asking for things, smallest first, and spend the user’s patience like it’s your own money.

Even the carousel offenders understand this on their better screens. Revolut’s “getting started” page skips abstractions and lists the actual things you can do, with a visible “Not now” escape, which respects the person more than any animation could. And the one slide in N26’s five that earns its place is the one showing the real Insights donut with real-looking numbers: the product itself, not a claim about it. If a marketing screen must exist, make it a screenshot of the future.

The pushback I get on this order is always compliance, and it’s usually softer than it sounds. Regulation says what you must collect; it rarely says when. In most of the flows I’ve rebuilt, the sequence was a habit somebody shipped years ago, not a legal requirement anyone could point to. Ask the legal team which steps genuinely have to happen before you can show someone their rate and their limit. The real list tends to be short, and everything not on it can move to after the moment the person has something to lose.

This is also where the two-second rule from my ads years applies hardest; I wrote about that separately in every screen is an ad. A KYC step is an ad for the step after it. If it can’t say what the person gets for completing it, it will bleed.

Revolut’s better screen: concrete things you can do, and a “Not now” escape

The one N26 slide that earns its place: the actual product, not a claim about it

A funnel is a series of moments

A funnel is a series of moments where someone decides you’re still worth their time. The apps that win treat each of those moments as the product. The apps that leak treat them as compliance homework between the marketing and the dashboard. If you take one thing from this note, audit your KYC flow with the same eyes you use on your landing page.

If you want to go deeper, these are worth your time:

- Built for Mars: Peter Ramsey’s UX teardowns, including a legendary series opening real bank accounts and counting every click

- Nielsen Norman Group on mobile onboarding: the research behind why front-loaded tutorials fail

- Growth.design case studies: comic-format teardowns of real onboarding funnels, including several fintechs

- Baymard on form fields: the evidence that most flows ask for roughly twice as much as they need

And for the health-app version of this argument, where the stakes are anxiety rather than money, read nobody wants a lab report.